Ghana’s banks held more in customer deposits than the government spent in 2025

- bernard boateng

- 1 day ago

- 2 min read

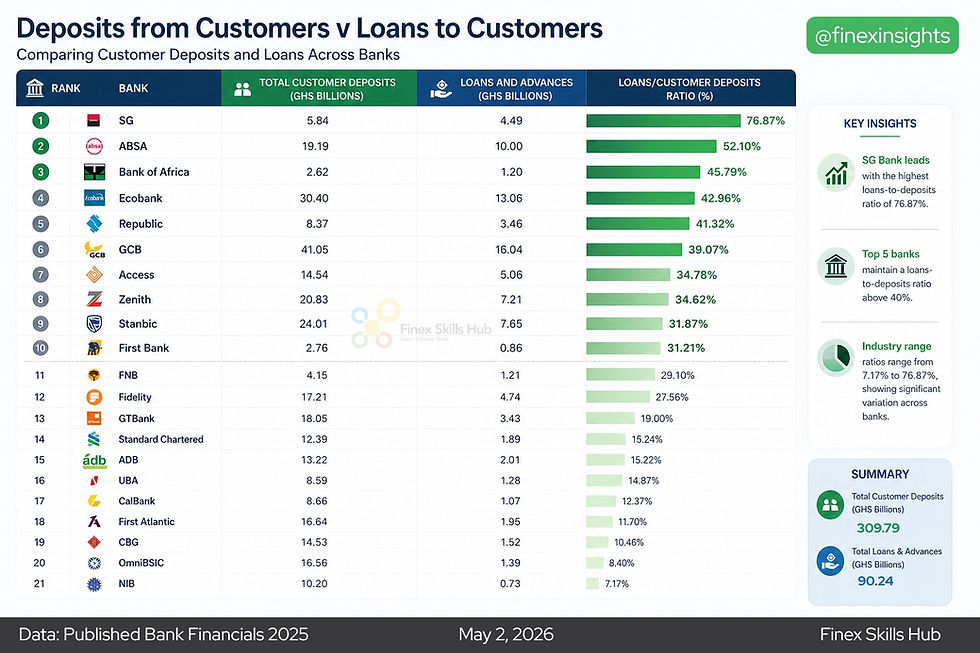

Ghana’s financial system is quietly revealing a powerful story, one that challenges how we typically think about money, influence, and economic control. In 2025, customer deposits held within Ghana’s banking sector (drawn from the Financial Statements of 21 banks) reached approximately GHS 309.79 billion, surpassing total government expenditure of GHS 233.78 billion for the same period. On the surface, this comparison is striking, but its deeper implications are even more important.

At its core, this contrast highlights the growing scale of financial intermediation in Ghana. Banks are increasingly acting as the central hubs of liquidity, holding vast pools of idle or semi-active capital. Meanwhile, government spending, though substantial, represents the structured deployment of funds toward public services, infrastructure, and economic stabilization. The fact that deposits exceed expenditure suggests that a significant portion of Ghana’s financial resources sits within the banking system rather than being actively circulated through fiscal channels.

However, it is important to understand that this is not a like-for-like comparison. Customer deposits represent a stock, a snapshot of accumulated funds at a given time, while government expenditure is a flow, measured over a full year. Despite this distinction, the comparison remains useful in illustrating scale and financial concentration.

One key implication is the question of financial efficiency. If banks are holding over GHS 300 billion in deposits, how much of this capital is being effectively transformed into productive lending? Are businesses and households accessing these funds in ways that drive economic growth, or is liquidity becoming trapped within the system? This raises broader concerns about credit access, interest rate structures, non-performing loan ratios and the risk appetite of financial institutions.

Another dimension is fiscal capacity. Government expenditure reflects policy priorities and economic intervention. When deposits significantly exceed public spending, it suggests that private sector liquidity may outweigh direct fiscal influence. In such a scenario, economic momentum may increasingly depend on how effectively banks deploy capital rather than how much the government spends.

Globally, similar patterns can be observed in more developed financial systems, where banking sector assets often exceed government budgets. However, in emerging economies like Ghana, the gap carries different implications. It can signal financial deepening, but it can also point to structural inefficiencies particularly if high liquidity does not translate into investment, job creation, or industrial expansion.

Ultimately, this insight is less about which figure is larger and more about what the relationship between them reveals. Ghana’s economy is evolving, with banks playing an increasingly dominant role in shaping financial flows. The real question is whether this growing pool of deposits is being harnessed effectively to support long-term economic transformation.

Comments