Why Ghana’s Banks Are Holding Back on Lending.

- bernard boateng

- May 2

- 3 min read

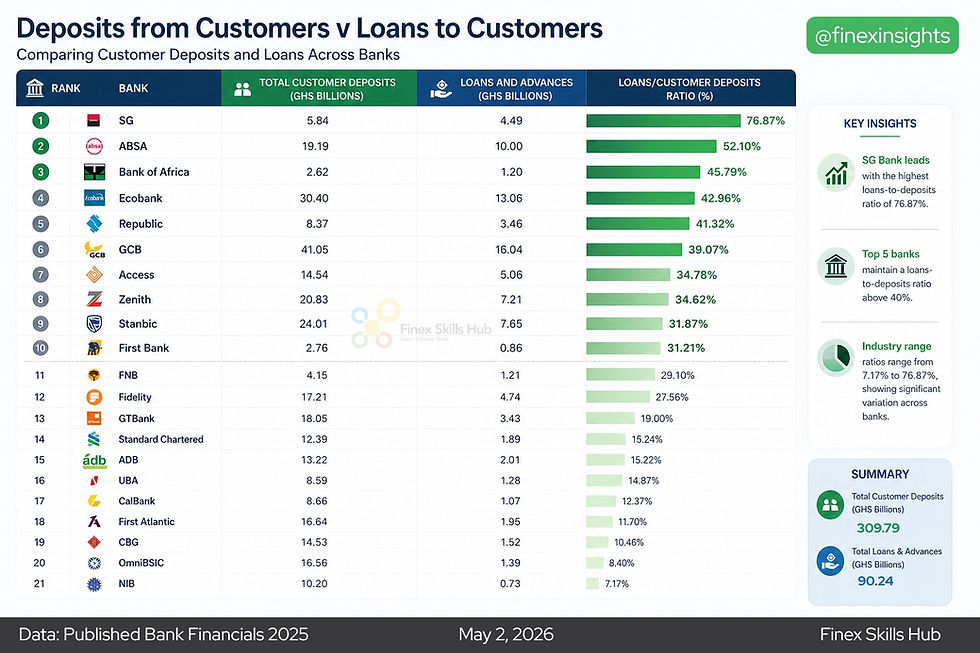

Ghana’s banking sector is sitting on a significant pool of liquidity. With total customer deposits reaching GHS 309.79 billion, the expectation would be that a substantial portion of these funds is being channeled into loans to support businesses and economic growth. But the data tells a more cautious story.

Across the industry, banks have extended only GHS 90.24 billion in loans and advances. This gap between deposits and lending reveals an important dynamic: banks are not deploying customer funds as aggressively as one might expect.

At the center of this conversation is the Loans-to-Deposits Ratio (LDR), a key metric used globally to assess how efficiently banks convert deposits into loans. In many markets, an LDR between 70% and 90% is considered healthy, striking a balance between profitability and liquidity risk.

In Ghana, however, the picture looks very different.

Only one bank crosses the 70% mark, with SG Bank leading at 76.87%. Beyond that, most banks fall significantly below global benchmarks. Several major institutions, despite holding large volumes of deposits, are lending less than half of what they could. For example, GCB Bank, the largest by deposits, records a loans-to-deposits ratio of just 39.07%, while Ecobank stands at 42.96%. This pattern suggests that scale is not necessarily translating into lending intensity.

What’s even more striking is the wide variation across banks. Ratios range from as high as 76.87% to as low as 7.17%, highlighting very different approaches to risk and capital deployment. Some banks appear willing to push their balance sheets further to generate returns, while others are clearly prioritizing caution.

This raises an important question: why are banks holding back?

Part of the answer lies in risk. Ghana’s banking sector has gone through a period of restructuring in recent years, with heightened attention on asset quality and capital adequacy. In such an environment, banks naturally become more conservative, tightening credit standards and being more selective about who they lend to.

At the same time, government securities present a compelling alternative. Treasury bills and bonds offer relatively high, low-risk returns, making them attractive compared to private sector lending. For many banks, the decision becomes less about how much they can lend and more about where they can achieve the best risk-adjusted returns.

The implication is clear: while banks are liquid, that liquidity is not fully translating into credit for businesses and individuals. This has broader consequences for the economy. Limited lending can slow private sector growth, restrict access to capital for small and medium-sized enterprises, and ultimately dampen economic expansion.

For customers, it also changes the narrative around deposits. The money held in bank accounts is not always being actively recycled into the economy through loans. Instead, a portion of it is being parked in safer instruments, reinforcing the sector’s cautious stance.

None of this suggests weakness. In fact, Ghana’s banking sector today is more stable and better capitalized than it has been in years. But stability often comes with conservatism. The real challenge going forward will be finding the right balance ensuring that banks remain prudent while also playing a more active role in financing economic growth.

Because ultimately, the health of a banking system is not just about how much it holds, but how effectively it puts those funds to work.

I was looking forward to a paragraph on NPL which probably one of the reasons why banks are cautious to lend